What Is the Difference Between a Mutual Fund Distributor (MFD) and a Registered Investment Advisor (RIA) in India?

The core distinction between a Mutual Fund Distributor (MFD) and a SEBI-registered Investment Advisor (RIA) in India lies in their regulatory framework, compensation model, and the nature of their obligation to the investor. While both can guide investors towards mutual funds, their underlying business models create fundamentally different relationships and potential cost implications.

Understanding these differences is paramount for investors seeking clarity on who truly offers unbiased advice versus product distribution. For a deeper dive into how these intermediaries are compensated, particularly the mechanics of trail commissions, refer to our comprehensive article on how mutual fund distributors earn trail commission in India.

How does a Mutual Fund Distributor (MFD) operate?

A Mutual Fund Distributor (MFD) acts as an intermediary, facilitating the purchase and sale of mutual fund units on behalf of investors. MFDs are primarily regulated by the Association of Mutual Funds in India (AMFI) and are compensated through commissions paid by the Asset Management Companies (AMCs) whose funds they distribute. These commissions are embedded within the Total Expense Ratio (TER) of the regular plan mutual funds they recommend. MFDs adhere to a 'suitability' standard, meaning they must recommend products suitable for the client's stated risk profile, but they are not legally bound to recommend the 'best' or lowest-cost option.

What defines a Registered Investment Advisor (RIA) in India?

A Registered Investment Advisor (RIA) is an individual or entity registered with the Securities and Exchange Board of India (SEBI) under the SEBI (Investment Advisers) Regulations, 2013. RIAs operate on a fee-only model, charging clients directly for their advice rather than earning commissions from fund houses. Crucially, RIAs are legally bound by a 'fiduciary duty', meaning they must always act in their clients' best interest, providing unbiased, holistic financial planning and recommending direct mutual fund plans, which have lower Total Expense Ratios (TERs) as they strip out distributor commissions.

How Do Mutual Fund Distributors and RIAs Charge for Their Services?

The charging mechanism forms the most significant structural difference between Mutual Fund Distributors (MFDs) and Registered Investment Advisors (RIAs), directly impacting an investor's net returns. MFDs receive commissions from fund houses, embedded in the Total Expense Ratio (TER) of regular plans, while RIAs charge a transparent fee directly to the client for their advice, recommending lower-cost direct plans.

What are the cost structures for MFD services?

MFDs primarily earn through trail commissions paid by Asset Management Companies (AMCs). These commissions are a percentage of the Assets Under Management (AUM) that the MFD brings in and maintains. This means that for every rupee invested through an MFD, a portion of the fund's expense ratio is paid to the distributor. According to SEBI circular SEBI/HO/IMD/DF2/CIR/P/2019/14 dated January 22, 2019, the difference in TER between direct and regular plans, which largely accounts for these commissions, can range from 0.50% to 1.10% annually, depending on the fund category. This cost is not explicitly stated to the investor but is deducted from the fund's Net Asset Value (NAV) daily.

How do RIAs charge for investment advice?

RIAs operate on a fee-only model, meaning they charge a transparent fee directly to their clients for the financial planning and investment advisory services provided. This fee can be a fixed amount, a percentage of the Assets Under Advice (AUA), or based on a specific project. Since RIAs do not earn commissions from AMCs, they recommend direct mutual fund plans, which have a lower Total Expense Ratio (TER) because they do not include distributor commissions. This fee structure eliminates conflicts of interest related to product selection, as the RIA's income is independent of the specific funds recommended.

Mutual Fund Distributor vs. Registered Investment Advisor: A Comparative Analysis

A direct comparison reveals the distinct operational and ethical frameworks governing Mutual Fund Distributors (MFDs) and Registered Investment Advisors (RIAs). These differences are critical for investors to understand when choosing a financial professional to guide their mutual fund investments.

| Feature | Mutual Fund Distributor (MFD) | Registered Investment Advisor (RIA) |

|---|---|---|

| Regulatory Body | AMFI (Association of Mutual Funds in India) | SEBI (Securities and Exchange Board of India) under SEBI (Investment Advisers) Regulations, 2013 |

| Business Model | Product distribution, transaction facilitation | Fee-only investment advice, financial planning |

| Compensation | Commissions from AMCs (embedded in Regular Plan TER) | Transparent fees charged directly to client (fixed, AUA-based, or project-based) |

| Fiduciary Duty | No (operates under suitability standard) | Yes (legally bound to act in client's best interest) |

| Investment Plan Type | Recommends Regular Plans (higher TER) | Recommends Direct Plans (lower TER) |

| Scope of Service | Primarily mutual fund product recommendations and transactions | Holistic financial planning, goal setting, portfolio construction, tax planning, beyond just mutual funds |

| Conflict of Interest | Potential for recommending funds with higher commissions | Minimised due to fee-only structure and fiduciary duty |

| Transparency of Cost | Indirect (embedded in TER, not explicitly paid by investor) | Direct and transparent (explicit fee paid by investor) |

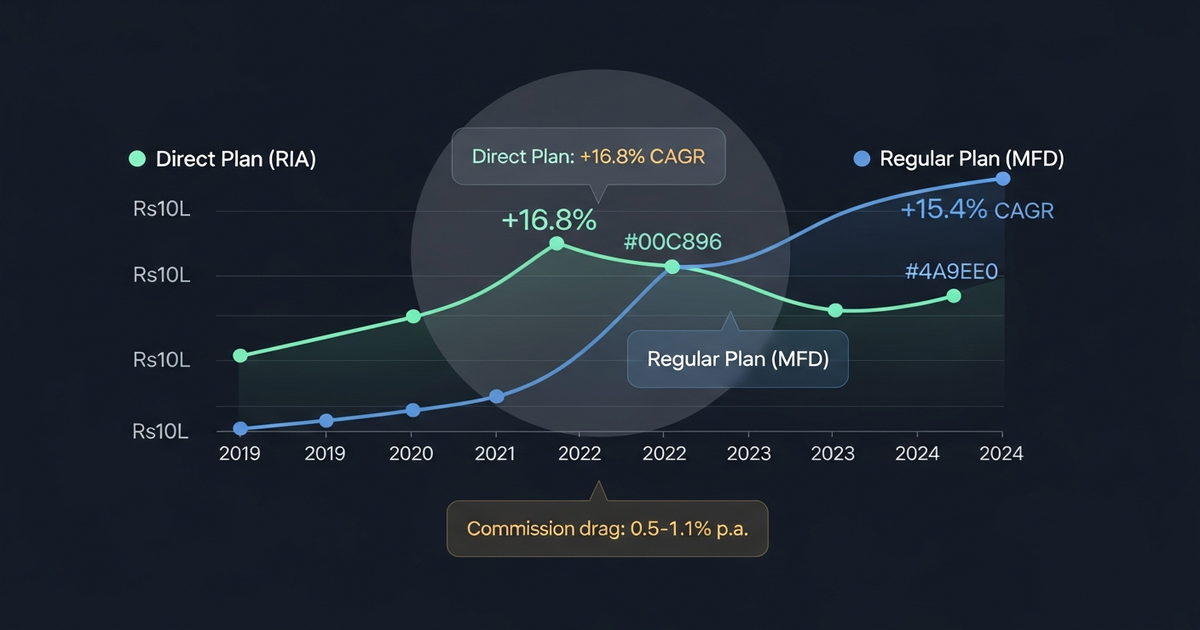

Quantifying the Cost Impact: MFD Regular Plan vs. RIA Direct Plan

The seemingly small difference in Total Expense Ratio (TER) between regular and direct mutual fund plans, typically ranging from 0.50% to 1.10% per annum, can lead to a substantial divergence in wealth accumulation over the long term. This is a critical factor for investors to consider, as it directly impacts their net returns.

What is the long-term impact of TER on your portfolio?

Consider an investor making a Systematic Investment Plan (SIP) of ₹10,000 per month for 20 years. Assuming a gross annualised return of 12% before expenses, we can project the difference in corpus between investing via a regular plan (with an illustrative TER of 1.75%) and a direct plan (with an illustrative TER of 0.75%). This 1.00% TER differential, while appearing minor annually, compounds significantly over two decades.

Free · No spam · Unsubscribe anytime

Learn investing without the jargon

Plain-English guides on MFs, SIPs, and taxes — one email a week, free forever.

Worked Example: SIP Corpus Projection (Illustrative)

- Monthly SIP: ₹10,000

- Investment Horizon: 20 years (240 months)

- Gross Annualised Return (before TER): 12.00%

- Illustrative Regular Plan TER: 1.75%

- Illustrative Direct Plan TER: 0.75%

| Plan Type | Effective CAGR (Net of TER) | Total Investment (20 Years) | Estimated Corpus After 20 Years | Cost Differential (Corpus Gap) |

|---|---|---|---|---|

| Regular Plan | 10.25% (12.00% - 1.75%) | ₹24,00,000 | ₹79,10,312 (Illustrative) | ₹13,29,788 |

| Direct Plan | 11.25% (12.00% - 0.75%) | ₹24,00,000 | ₹92,40,100 (Illustrative) |

Note: Figures are illustrative and based on assumed TERs and CAGR for a well-known fund like Parag Parikh Flexi Cap Fund. Actual returns and TERs may vary.

As evident from the projection, the 1.00% annual TER difference results in a substantial corpus gap of over ₹13 lakh over 20 years. This demonstrates the powerful effect of compounding costs and highlights why understanding TER and choosing the right investment channel is crucial for long-term wealth creation.

Analyse This on BullWiser — Free

BullWiser's MF Analyser surfaces TER drag, BullWiser Score, Sharpe Ratio, Alpha, Beta, and rolling returns for any Indian mutual fund. Compare funds side by side or upload your CAS statement to diagnose your full portfolio's weighted expense load and overlap.

Open BullWiser MF Analyser →Common Misconceptions About Financial Advisors in India

Many investors hold preconceived notions about financial advisors, which can sometimes lead to suboptimal investment decisions. Dispelling these myths with data and regulatory facts is crucial for making informed choices.

Do MFDs always recommend the best-performing funds?

A common misconception is that MFDs consistently recommend the 'best-performing' funds. While MFDs are expected to recommend suitable funds, their primary incentive structure is commission-based, which can, at times, create a conflict of interest. Funds that offer higher trail commissions might inadvertently receive more prominence, regardless of their long-term performance consistency or efficiency in terms of Total Expense Ratio (TER). The 'best' fund is subjective and depends on individual goals, risk appetite, and cost efficiency, not solely on past returns. Investors should always verify fund performance and TER independently using tools like the BullWiser MF Analyser.

Is a "free" MFD service truly without cost?

The idea that an MFD's service is 'free' is a pervasive myth. While investors do not pay an explicit fee directly to the MFD, the cost is implicitly borne through the higher Total Expense Ratio (TER) of regular mutual fund plans. The difference in TER between regular and direct plans, typically 0.50% to 1.10% annually, represents the distributor's commission. This 'hidden' cost is deducted from the fund's Net Asset Value (NAV) daily, eroding returns over time. Therefore, the service is never truly free; the cost is simply structured differently and less transparently than a direct fee.

Are RIAs only for high net worth individuals?

Another misconception is that Registered Investment Advisors (RIAs) cater exclusively to High Net Worth Individuals (HNIs). While RIAs historically attracted larger clients due to their fee structures, many RIAs today offer services to a broader range of investors, including those with smaller portfolios or specific financial planning needs. The value an RIA provides through unbiased, fiduciary advice and access to lower-cost direct plans can be significant for any investor, regardless of portfolio size, especially over long investment horizons where compounding savings from lower TERs become substantial. The focus should be on the value of advice and cost efficiency, not just portfolio size.

Frequently Asked Questions About MFDs and RIAs

What is the main difference in how MFDs and RIAs are regulated?

The main difference is in their regulatory bodies and duties. MFDs are primarily governed by AMFI and act as agents of mutual fund houses, earning commissions. RIAs, however, are regulated directly by SEBI under the SEBI (Investment Advisers) Regulations, 2013, and must adhere to a strict fiduciary duty. This ensures RIAs provide unbiased advice.

Does using an MFD cost me more than an RIA?

Generally, yes, using an MFD can cost you more over the long term. MFDs typically recommend regular mutual fund plans, which have a higher Total Expense Ratio (TER) due to embedded commissions. RIAs, conversely, recommend direct plans with lower TERs and charge a transparent fee directly to you. This difference in TER, often 0.50% to 1.10% annually, compounds significantly. The lower TER of direct plans can lead to substantial savings.

Can an MFD also act as an RIA?

No, an individual or entity cannot simultaneously act as both a Mutual Fund Distributor (MFD) and a Registered Investment Advisor (RIA) for the same client. SEBI regulations (SEBI/HO/IMD/DF2/CIR/P/2019/14 dated January 22, 2019) explicitly prohibit this to avoid conflicts of interest. An advisor must choose one role to maintain clarity and adhere to regulatory frameworks. This separation ensures that advice is either fee-based or commission-based, but not both.

What is "fiduciary duty" for an investment advisor?

Fiduciary duty means an RIA is legally and ethically bound to act in their client's absolute best financial interest, placing the client's needs above their own. This includes providing unbiased advice, recommending suitable investments, and disclosing any potential conflicts of interest. It's a higher standard of care compared to the suitability standard that MFDs typically follow. An RIA must always put your interests first.

Why do RIAs recommend direct plans?

RIAs recommend direct plans because they are legally obligated to act in their clients' best interest, and direct plans have a lower Total Expense Ratio (TER) compared to regular plans. This lower TER translates to higher net returns for the investor over time, as there are no embedded distribution commissions. It aligns with their fiduciary duty to minimise costs for the client. Direct plans offer better value for the investor.

How do I verify if an advisor is SEBI-registered?

You can verify if an advisor is SEBI-registered by visiting the official SEBI website. SEBI maintains a comprehensive list of all Registered Investment Advisers, including their registration number and contact details. This ensures you are dealing with a legitimate and regulated professional. Always check the SEBI portal for verification before engaging with any investment advisor.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice or a solicitation to transact in any security. Mutual fund investments are subject to market risks. Past performance is not indicative of future returns. All regulatory data referenced is subject to change — verify current SEBI and AMFI guidelines on official sources. Consult a SEBI-registered investment adviser before making any financial decision.

For a complete list of SEBI-registered investment advisers, visit the official SEBI portal: SEBI Registered Investment Advisers.